Sharpe ratio in finance is named after Nobel laureate William. S.Sharpe

Sharpe ratio is a measurement of risk adjusted return of a portfolio or a particular stock or a trading account or trading system

Sharpe ratio can be calculated as below

Sharpe ratio = (Portfolio return – Risk free return)/portfolio standard deviation of return.

Risk free return is usually long term G-SEC bond return and it is around 6.8 to 7% in this example.

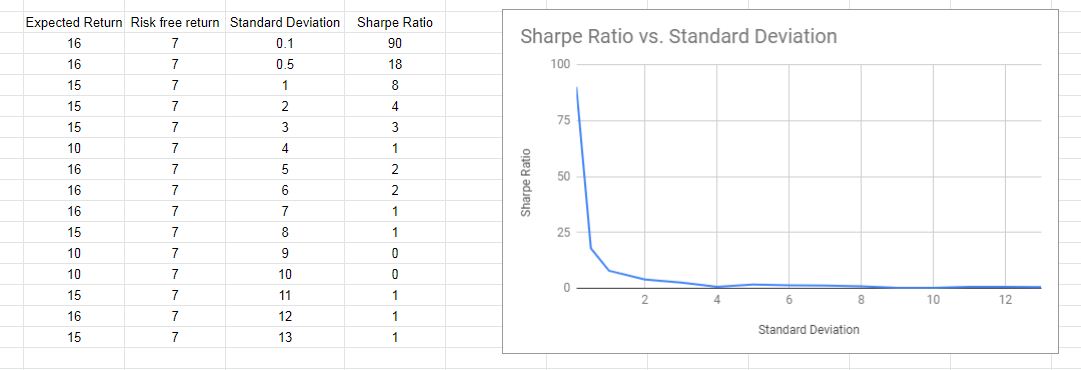

This is illustrated below

From the chart one can see, if the portfolio standard deviation is more, the sharpe ratio is decreasing and vice-versa. Positive sharpe ratio is used as a performance metric.

Sharpe ratio >1 is considered good, >2 is very good, > 3 is great

In simple terms, for any risk taken for an investment, your investment should give good returns at the least greater than the risk free return.